The Local Government Funding Agency (LGFA) wants to branch out to provide finance to Ratepayers who can’t afford to pay their rates.

The Local Government Funding Agency (LGFA) wants to branch out to provide finance to Ratepayers who can’t afford to pay their rates.

Is that something we think a consortium of Central and Local Government entities should be providing finance for ?

Is that something we think the Government should consult people about before it is put in place ?

We didn’t go looking for this story – it was an unexpected link in something else we were looking at, but the more we looked at who was involved with this proposed scheme the more we don’t like the “product” being developed for people who can’t afford to pay their rates.

Rates have increased way too much and a lot of Ratepayers are now struggling to pay them. Rather than the Government heavily focusing on bringing rates down, and stopping unnecessary spending, one of the products in this scheme gets Ratepayers in to debt as a way to pay their rates so they can keep their home (in the short term anyway).

A consortium of Local Government NZ (a private business), the Central Government, a few local Councils, a few other Government Departments, and an NZ Investment Banking Company with a longstanding relationship with the Rothschilds Investment Bank in the US, are working on a scheme to offer finance to Ratepayers.

**Who is behind the development of this proposed scheme is listed at the end**

This has not been approved by Central Government yet, but this is being proposed to be in place later in 2026.

There has been a scheme running with the NZ Government called the Ratepayers Assistance Schemes (RAS) where the Government (the Taxpayers of NZ) covered the cost of people who couldn’t afford to pay their rates.

The Minister of Local Government, Simon Watts, has asked the group behind the RAS scheme to refresh a business case, to remove the cost of this scheme from the Central Government, provide finance direct to ratepayers through the LGFA, so Councils get paid up front and homeowners can borrows money over a long timeframe, in an attempt to keep up with paying their rates.

Obviously, this scheme will cost those ratepayers more than the cost of their rates as they will also be paying interest on the money they borrow. How anyone could promote a scheme like this as beneficial for a ratepayer by making their rates “more affordable” is nonsense.

The NZ Government and interested Councils across the country will be shareholders of this new scheme. All Councils across NZ are currently being asked by LGNZ to express their interest in putting money in to the scheme and becoming a shareholder. In the case of Hutt City Council in Wellington, $2.5M is the amount they need to invest to become a shareholder. It would seem that $2.5M would be money from rates income, or would it be debt on behalf of Ratepayers ?

So, the Government and Councils are the shareholders of a scheme which lends out money, a profit is made from the interest rates charged, and the shareholders will share in any of those profits.

Why are the NZ Government and Councils so keen to run businesses that profit from taxpayers and ratepayers ?

“Products” that would not be needed if rates had not increased so much in the last 10+ years.

For Ratepayers struggling to pay their rates, this scheme is like the Heartland Bank reverse mortgage product. An option that already exists where the private business carries all the risk if things go wrong.

The LGFA cost of living crisis “product” will compete with NZ private business to offer lower rates for people in trouble financially. The websites promoting this concept to Councils think it is a great product as “you don’t need to worry about not being able to pay your rates”. But you will be very concerned once your house is sold and the money has to be paid back and very little equity is left in the home.

We are aware of many superannuants in New Plymouth who have rates which have increased to $14k plus a year who are trying to pay this from a total income of a $21k pension (per person). These people would very quickly owe the Government a very large sum of money to keep up with paying their rates.

Borrowing money to keep up with paying rates is not an answer any ratepayer, anywhere, needs.

General rules with financing is to avoid lending money to people who can’t afford to pay it back - if you want a sustainable finance company. And yes, the idea here is that the future value of the house will pay back the loans not paid, but house markets go up and down, and sometimes crash unexpectedly.

Wasn’t the 2008 Global crash connected to lending from investment banks in property markets to people who couldn’t afford to pay ?

We don’t need an option to borrow money to pay rates, we need a Government and Councils who make sure rates become affordable again.

The other “product” in this scheme – which is for property developers’ upfront costs and home improvements for things like Solar Power – this could be quite beneficial in helping some projects go ahead due to lower interest rates than the NZ Banks offer, and lending terms which go 20 to 30 years, for smaller amounts than a mortgage.

But why are the Government and the Councils the shareholders ? If this scheme is beneficial why aren’t shareholders being sought from the public and private investment, who will carry the risks as well as the benefits.

And, why is this not being discussed with Ratepayers BEFORE Councils decide they want to get on board as a shareholder.

As this is at a business case stage there is no fine print available of whether the Ratepayers across the country will also be the guarantors of these new types of loans. It is not obvious where the money comes from that is lent out by the Government, but if any form of Investment Bank provides these funds, whether from NZ or the US, then we strongly believe that those investment banks should carry all the risks if their business model should fail at any point.

We will keep an eye on how these new options for the LGFA progress through 2026 and keep you posted.

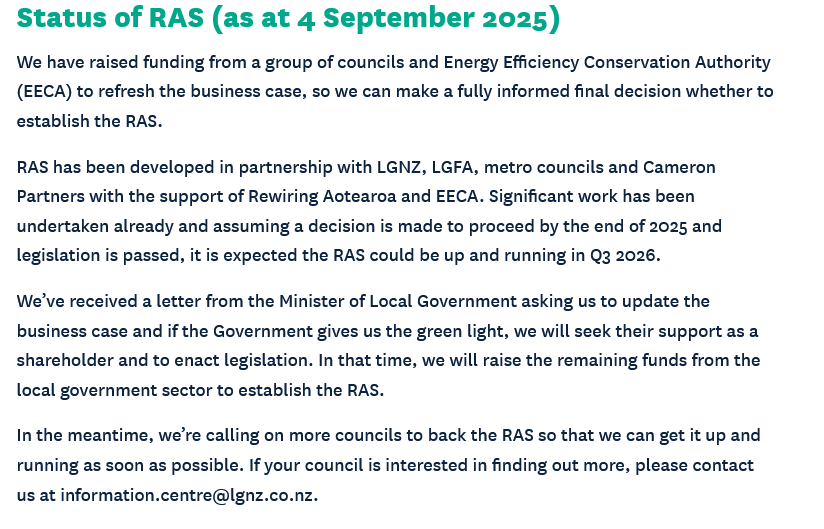

The picture attached is from the LGNZ website with the current Status of the Rates Assistance Scheme.

** Who is involved with the updated version of the Ratepayer Assistance Scheme (RAS)

- What was the Ratepayers Assistance Scheme (RAS) – now called Rewiring Aotearoa

- A government Department EECA – Energy Efficiency Conservation Authority

- LGNZ – Local Government NZ (a private business funded by many NZ Councils)

- LGFA – Local Government Funding Agency (The Central Government and 18 NZ Councils who lend money to NZ Councils. Ratepayers guarantee all the loans across the country for this organisation).

- A group of metro Councils (It is not mentioned who these are)

- Cameron Partners (An NZ investment Banking firm with a long-standing alliance with Rothschild & Co – a very long-standing American Investment Banking Company).

Links to Websites:

LGNZ Ratepayer Assistance Scheme

https://www.lgnz.co.nz/policy-advocacy/ratepayer-assistance-scheme/

Rewiring NZ website

Cameron Partners - An NZ investment Banking firm with a long-standing alliance with Rothschild & Co

https://cameronpartners.co.nz/

Posted: Sun 11 Jan 2026